Market Making & Microstructure Research Platform

GitHubOverview

Research framework for market making as a coupled system of alpha, execution, inventory, and regime-dependent liquidity provision.

Built for live L2 market data, deterministic replay, and execution-aware signal evaluation.

Built for live L2 market data, deterministic replay, and execution-aware signal evaluation.

Core Insight

Market making is not a forecasting problem.

It is a conditional execution problem under microstructure constraints:

- alpha identifies where edge exists

- regimes determine when edge is valid

- toxicity determines whether liquidity should be provided

- execution determines whether edge is realized

- fees + queue dynamics determine whether edge survives

Most theoretical edge is lost through execution and adverse selection, not prediction error.

It is a conditional execution problem under microstructure constraints:

- alpha identifies where edge exists

- regimes determine when edge is valid

- toxicity determines whether liquidity should be provided

- execution determines whether edge is realized

- fees + queue dynamics determine whether edge survives

Most theoretical edge is lost through execution and adverse selection, not prediction error.

System Overview

Market Data / Replay

│

▼

Order Book State

│

▼

Regime Detection (GMM clustering)

│

▼

Alpha Stack

├─ Microstructure Alpha (fast signal)

├─ Structural Alpha (slow microstructure)

└─ ML Residual Alpha (XGBoost correction)

│

▼

Toxicity Model (expected markout)

│

▼

Quote / Skew / Size Decision

│

▼

Execution Model (queue + cancellations + fees)

│

▼

Inventory / Risk

│

▼

Dataset Generation & Research

Supports:

- live trading

- paper trading

- full historical replay

│

▼

Order Book State

│

▼

Regime Detection (GMM clustering)

│

▼

Alpha Stack

├─ Microstructure Alpha (fast signal)

├─ Structural Alpha (slow microstructure)

└─ ML Residual Alpha (XGBoost correction)

│

▼

Toxicity Model (expected markout)

│

▼

Quote / Skew / Size Decision

│

▼

Execution Model (queue + cancellations + fees)

│

▼

Inventory / Risk

│

▼

Dataset Generation & Research

Supports:

- live trading

- paper trading

- full historical replay

Regime Model

Unsupervised Gaussian Mixture Model (GMM) using:

- volatility

- spread

- order imbalance

- trade imbalance

- quote churn

- inventory

- inventory volatility

- microprice error

Results:

- discrete market regimes with materially different alpha expression.

Key observations:

- regimes gate alpha effectiveness rather than generate edge.

- volatility

- spread

- order imbalance

- trade imbalance

- quote churn

- inventory

- inventory volatility

- microprice error

Results:

- discrete market regimes with materially different alpha expression.

Key observations:

- regimes gate alpha effectiveness rather than generate edge.

Alpha Stack

1. Microprice Alpha

Top-of-book imbalance signal.

- strongest at 100 - 500ms horizons

- captures immediate order book pressure

- fast-decaying but directionally informative

2. Structural Alpha

Slower microstructure signal:

- volatility

- order/trade imbalance

- inventory pressure

- microprice deviation

More stable estimate of short-horizon fair value than microprice alone.

3. Residual ML (XGBoost)

Learns residual drift after structured fair value:

- weak short-horizon signal

- improves at 1 - 5s horizons

- acts as correction layer, not primary alpha

Top-of-book imbalance signal.

- strongest at 100 - 500ms horizons

- captures immediate order book pressure

- fast-decaying but directionally informative

2. Structural Alpha

Slower microstructure signal:

- volatility

- order/trade imbalance

- inventory pressure

- microprice deviation

More stable estimate of short-horizon fair value than microprice alone.

3. Residual ML (XGBoost)

Learns residual drift after structured fair value:

log(mid_{t+h} / fair_value_t)

Behavior:- weak short-horizon signal

- improves at 1 - 5s horizons

- acts as correction layer, not primary alpha

Toxicity Model (Execution Risk)

Predicts expected markout conditional on execution:

- imbalance

- spread

- volatility

- microprice deviation

- inventory pressure

- queue position

Outputs:

- negative → toxic liquidity

- positive → favorable execution

Role:

- execution gating / participation filter

- used for skewing and size adjustment

Results:

- strong short-horizon predictability of adverse selection

- improves execution quality more than standalone PnL

T(x) = E[future markout_h ∣ fill, state]

Inputs:- imbalance

- spread

- volatility

- microprice deviation

- inventory pressure

- queue position

Outputs:

- negative → toxic liquidity

- positive → favorable execution

Role:

- execution gating / participation filter

- used for skewing and size adjustment

Results:

- strong short-horizon predictability of adverse selection

- improves execution quality more than standalone PnL

Execution Model

1. Fill Model

Passive fill modeled as stochastic Poisson queue depletion:

- trade-driven depletion

- cancellation-driven depletion (explicitly modeled)

Key correction:

- queue reduction is not equivalent to executed volume

2. Cost Model

- fees + turnover materially impact viability

- small execution inefficiencies dominate marginal signal gains

3. Latency Model

Execution timing significantly affects realized outcomes.

Future work:

- order placement latency

- cancellation latency

- exchange acknowledgement delays

Passive fill modeled as stochastic Poisson queue depletion:

P(fill) = 1 − exp(−(λ_t / Q_t) ⋅ Δ_t)

Includes:- trade-driven depletion

- cancellation-driven depletion (explicitly modeled)

Key correction:

- queue reduction is not equivalent to executed volume

2. Cost Model

PnL = spread capture + alpha − fees − adverse selection − slippage

Key implications:- fees + turnover materially impact viability

- small execution inefficiencies dominate marginal signal gains

3. Latency Model

Execution timing significantly affects realized outcomes.

Future work:

- order placement latency

- cancellation latency

- exchange acknowledgement delays

Inventory Model

Inventory treated as a continuous risk state.

Reservation price adjusts based on:

- inventory level

- volatility

- regime

Objective:

- balance spread capture vs directional exposure under changing conditions.

Reservation price adjusts based on:

- inventory level

- volatility

- regime

Objective:

- balance spread capture vs directional exposure under changing conditions.

Key Results

1. Alpha hierarchy is stable

- structural alpha > microprice > residual ML (short horizon)

2. Regimes improve selection, not edge

- reduce drawdowns

- improve consistency

- do not independently generate alpha

3. Toxicity is execution-side signal

- strong markout predictability

- improves fill quality

- can reduce PnL if overused (over-filtering)

4. Execution dominates marginal alpha gains

- queue dynamics + cancellations + fees significantly alter outcomes

- naive alpha materially degrades under realistic execution

- structural alpha > microprice > residual ML (short horizon)

2. Regimes improve selection, not edge

- reduce drawdowns

- improve consistency

- do not independently generate alpha

3. Toxicity is execution-side signal

- strong markout predictability

- improves fill quality

- can reduce PnL if overused (over-filtering)

4. Execution dominates marginal alpha gains

- queue dynamics + cancellations + fees significantly alter outcomes

- naive alpha materially degrades under realistic execution

Edge Decomposition

Market making performance decomposes into:

- alpha: where edge exists

- regime: when edge is valid

- toxicity: whether to participate

- execution: whether edge is realized

- fees: whether edge survives

- latency: how fast edge is captured

- alpha: where edge exists

- regime: when edge is valid

- toxicity: whether to participate

- execution: whether edge is realized

- fees: whether edge survives

- latency: how fast edge is captured

Core Takeaway

Market making performance decomposes into:

- alpha: where edge exists

- regime: when edge is valid

- toxicity: whether to participate

- execution: whether edge is realized

- fees: whether edge survives

- latency: how fast edge is captured

- alpha: where edge exists

- regime: when edge is valid

- toxicity: whether to participate

- execution: whether edge is realized

- fees: whether edge survives

- latency: how fast edge is captured

Live Execution (Binance Futures Testnet)

The platform includes a full live execution layer on Binance Futures Testnet, closing the loop from signal generation → quoting → execution → fills → PnL, and validating microstructure assumptions against real exchange behavior.

Execution Stack

Broker Layer (BinanceBroker)

- REST order placement/cancel with HMAC authentication

- user data stream (listenKey) for order lifecycle tracking

- position reconciliation via positionRisk

- session keepalive and recovery handling

Execution Engine (LiveExecution)

- inventory- and volatility-adjusted asymmetric quoting

- toxicity-aware participation and sizing

- queue-aware cancel/replace logic

- real-time trade-flow ingestion for state updates

User Stream Handler (BinanceUserStream)

- WebSocket ORDER_TRADE_UPDATE processing

- handles NEW / TRADE / CANCELED / REJECTED states

- maintains queue position estimates at entry

- synchronizes internal execution state with exchange events

Execution Stack

Broker Layer (BinanceBroker)

- REST order placement/cancel with HMAC authentication

- user data stream (listenKey) for order lifecycle tracking

- position reconciliation via positionRisk

- session keepalive and recovery handling

Execution Engine (LiveExecution)

- inventory- and volatility-adjusted asymmetric quoting

- toxicity-aware participation and sizing

- queue-aware cancel/replace logic

- real-time trade-flow ingestion for state updates

User Stream Handler (BinanceUserStream)

- WebSocket ORDER_TRADE_UPDATE processing

- handles NEW / TRADE / CANCELED / REJECTED states

- maintains queue position estimates at entry

- synchronizes internal execution state with exchange events

Key Live Findings

1. Latency is structural (~600-700ms end-to-end)

signal → execution exhibits latency dominated by REST gateway, network RTT, and WebSocket propagation

latency is a first-order state variable; it must be explicitly modeled in fill probability and queue dynamics

2. Market data is asynchronous (~150-300ms bursty updates)

order book updates arrive in event-driven bursts rather than fixed intervals due to batched WebSocket delivery

L2 data is intrinsically irregular; fixed-timestep assumptions distort microstructure inference

3. Execution dominates signal quality

queue position, cancellation timing, and latency differentials materially affect realized outcomes

most theoretical alpha is reshaped by execution mechanics rather than prediction error

4. Alpha-execution decomposition holds in practice

alpha identifies directional bias, toxicity captures adverse selection risk, and execution determines realized PnL

short-horizon variance is dominated by execution noise rather than signal quality

5. Queue state is first-class signal

queue position, cancellation dynamics, and trade-driven depletion are primary drivers of fill probability

validates explicit modeling of queue-ahead, cancellation resets, and trade-flow-based depletion

signal → execution exhibits latency dominated by REST gateway, network RTT, and WebSocket propagation

latency is a first-order state variable; it must be explicitly modeled in fill probability and queue dynamics

2. Market data is asynchronous (~150-300ms bursty updates)

order book updates arrive in event-driven bursts rather than fixed intervals due to batched WebSocket delivery

L2 data is intrinsically irregular; fixed-timestep assumptions distort microstructure inference

3. Execution dominates signal quality

queue position, cancellation timing, and latency differentials materially affect realized outcomes

most theoretical alpha is reshaped by execution mechanics rather than prediction error

4. Alpha-execution decomposition holds in practice

alpha identifies directional bias, toxicity captures adverse selection risk, and execution determines realized PnL

short-horizon variance is dominated by execution noise rather than signal quality

5. Queue state is first-class signal

queue position, cancellation dynamics, and trade-driven depletion are primary drivers of fill probability

validates explicit modeling of queue-ahead, cancellation resets, and trade-flow-based depletion

Updated Core Takeaway (Reinforced)

Market making is not constrained by predictive signal quality.

It is constrained by:

- latency uncertainty

- queue position randomness

- execution path dependence

- regime-dependent liquidity fragility

In live conditions, execution dynamics dominate alpha, and the primary optimization problem becomes:

- selective participation under microstructure and latency constraints, not prediction.

It is constrained by:

- latency uncertainty

- queue position randomness

- execution path dependence

- regime-dependent liquidity fragility

In live conditions, execution dynamics dominate alpha, and the primary optimization problem becomes:

- selective participation under microstructure and latency constraints, not prediction.

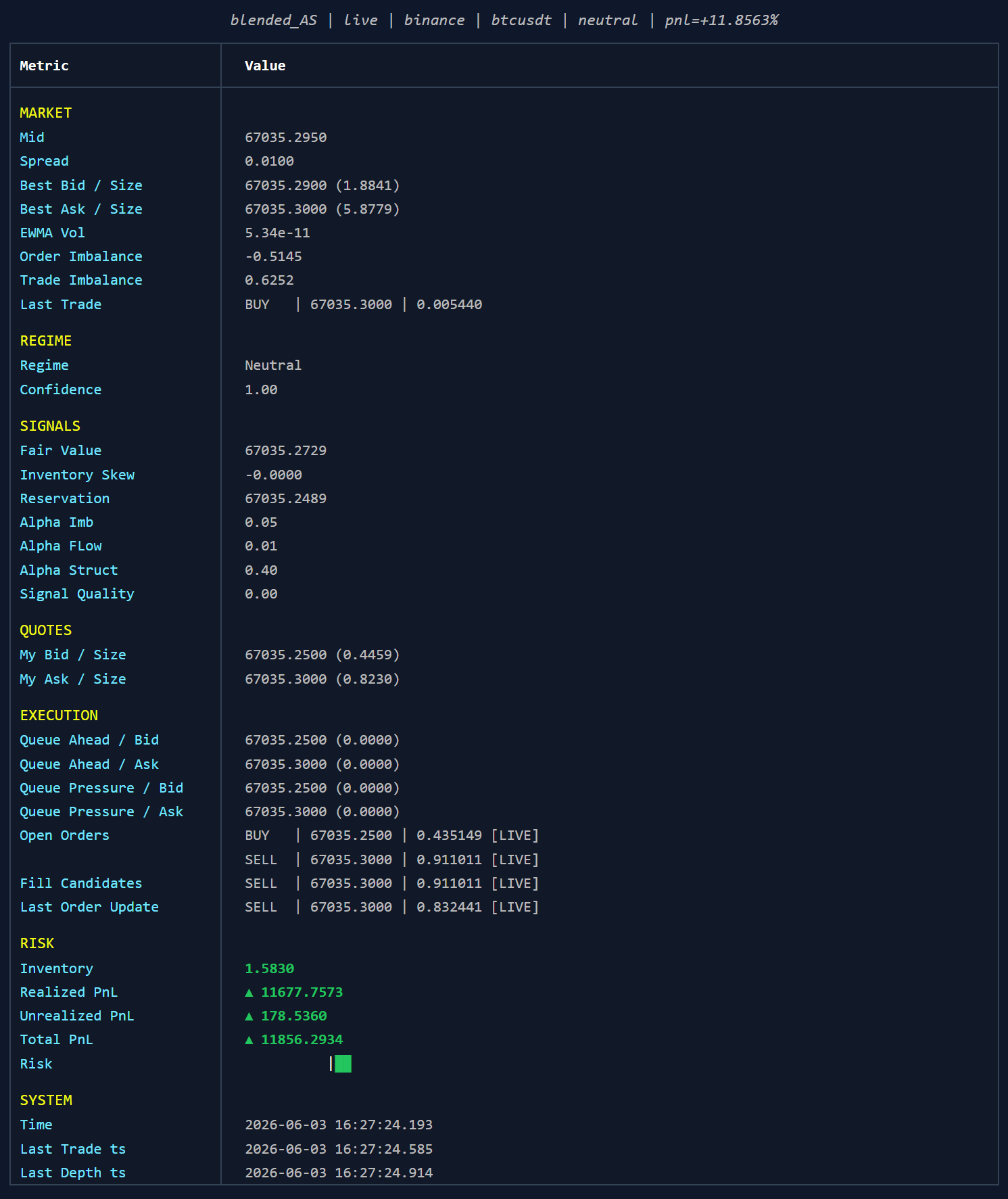

Trading Engine Visualizations

Trading terminal dashboard with live L2 market feed, regime detection, quoting strategy, and risk management.

Live L2 Binance Feed

Continuous updates of quotes, inventory, and market state under streaming data

Real-time microstructure execution engine

Visualizing order flow, queue state, and execution-driven PnL updates

.png)