Monte Carlo Decision Engine - Adversarial Sequential Decision Simulator

GitHubTrading Problem

Trading decisions are made under uncertainty, where outcomes depend on future stochastic states and adversarial behavior.

Core Idea

Actions are evaluated by simulating forward outcome distributions and selecting based on risk-adjusted expected value rather than point estimates.

Decision Logic

Each decision is scored using:

- Expected value (EV)

- Outcome distribution (risk / downside exposure)

- Sensitivity to stochastic state changes

- Expected value (EV)

- Outcome distribution (risk / downside exposure)

- Sensitivity to stochastic state changes

Trading Mapping

This models core prop trading dynamics:

- Sequential position sizing under uncertainty

- Adversarial market participant behaviorPath-dependent PnL evolution

- Risk-adjusted decisioning under incomplete information

- Sequential position sizing under uncertainty

- Adversarial market participant behaviorPath-dependent PnL evolution

- Risk-adjusted decisioning under incomplete information

Key Insights

- Decision quality depends on outcome distribution, not just EV

- Risk-adjusted evaluation improves robustness under uncertainty

- Sequential dependency amplifies exposure to state uncertainty

- Optimal actions are sensitive to changes in underlying assumptions

- Risk-adjusted evaluation improves robustness under uncertainty

- Sequential dependency amplifies exposure to state uncertainty

- Optimal actions are sensitive to changes in underlying assumptions

Why Monte Carlo?

Closed-form solutions are infeasible due to:

- Combinatorial state explosion

- Hidden information

- Multi-agent interactions

- Path-dependent outcomes

Monte Carlo enables scalable approximation of:

- Expected outcomes

- Risk distributions

- Decision robustness under uncertainty

- Combinatorial state explosion

- Hidden information

- Multi-agent interactions

- Path-dependent outcomes

Monte Carlo enables scalable approximation of:

- Expected outcomes

- Risk distributions

- Decision robustness under uncertainty

System Capabilities

- 10,000+ rollouts per decision

- Stochastic multi-agent simulation

- Sequential state evolution

- Risk-weighted decision selection (drawdown-aware)

- Stochastic multi-agent simulation

- Sequential state evolution

- Risk-weighted decision selection (drawdown-aware)

Core Takeaway

Trading decisions are evaluated through simulated outcome distributions and risk-adjusted expected value under stochastic and adversarial conditions.

Stochastic Decision-Making & Simulation Outputs

Benchmarks and system outputs demonstrating Monte Carlo-based decision evaluation, multi-agent interaction dynamics, and state evolution under risk constraints and incomplete information.

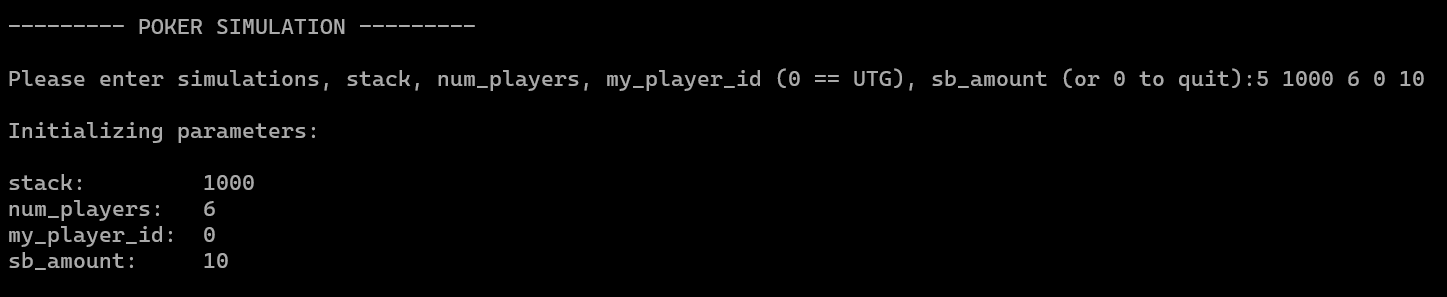

System Initialization for Sequential Decision Simulation

C++ engine initializing market-like state variables including agent capital, stack distribution, and simulation parameters for probabilistic outcome evaluation.

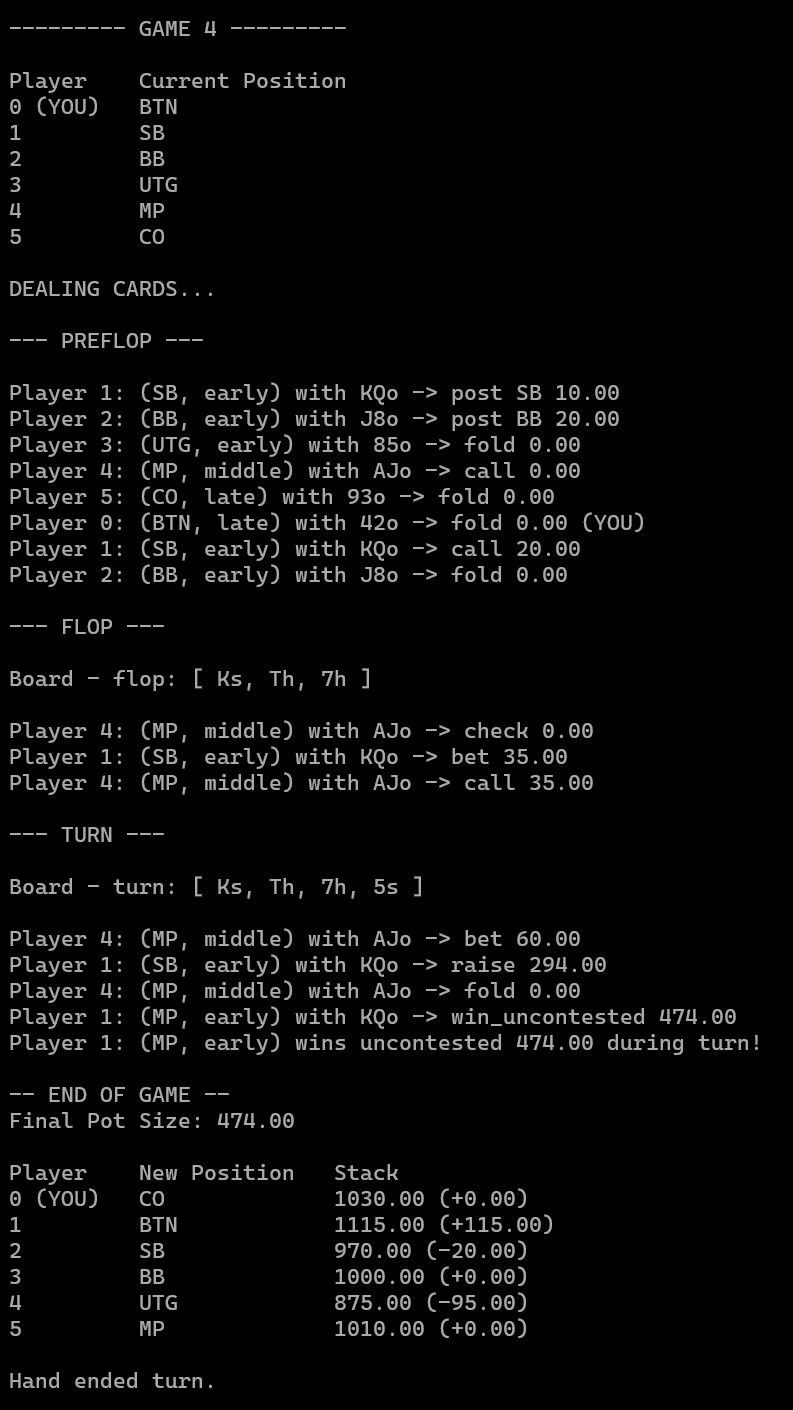

End-to-End Multi-Agent Simulation with Capital Evolution and Depletion Dynamics

Full Monte Carlo rollout capturing interaction effects, competitive pressure, and capital decay under adversarial decision environments.

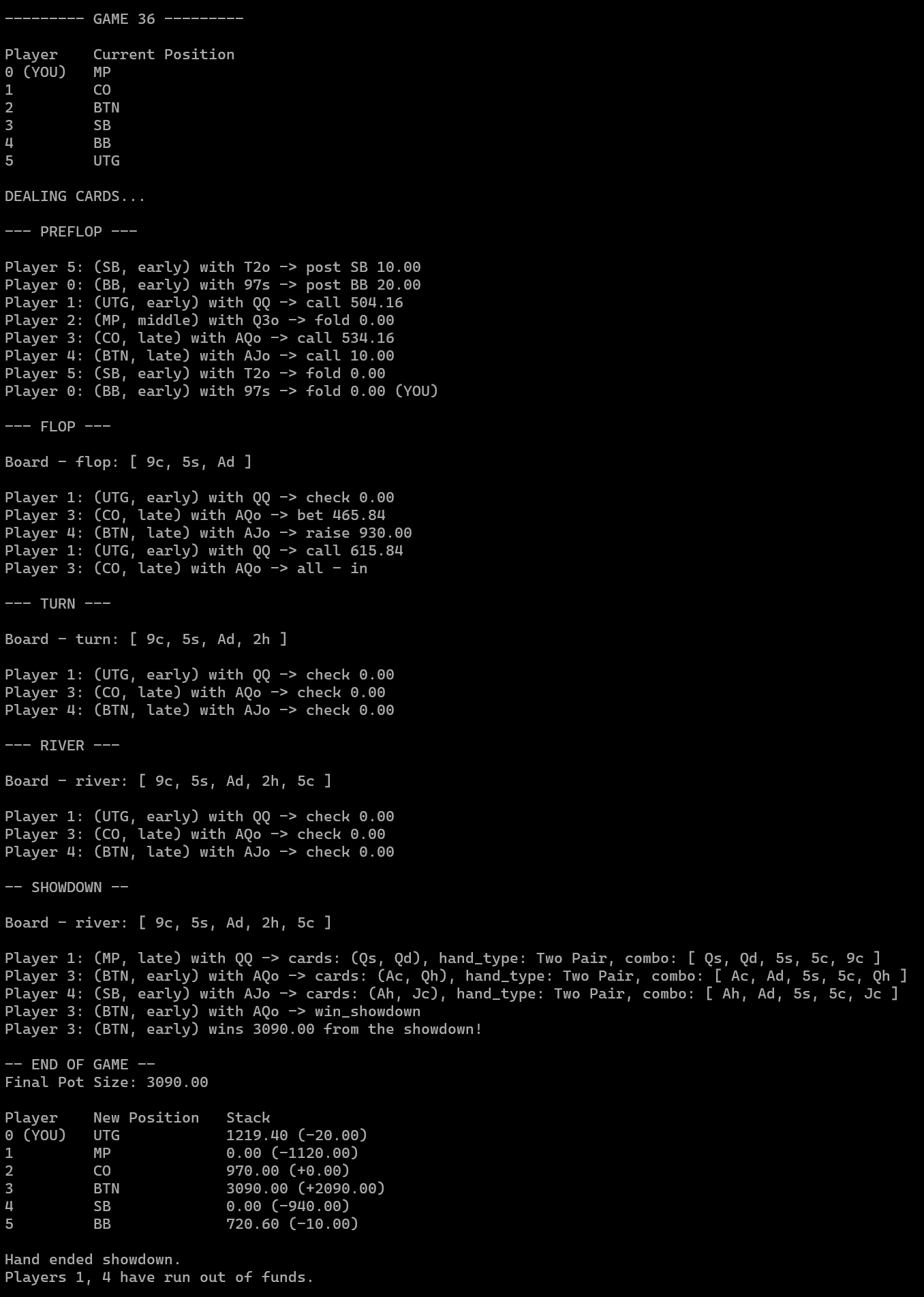

Absorbing State Event: Market Participant Elimination under Capital Depletion

Simulation state illustrating survival dynamics and path-dependent risk of ruin under sequential decision pressure.

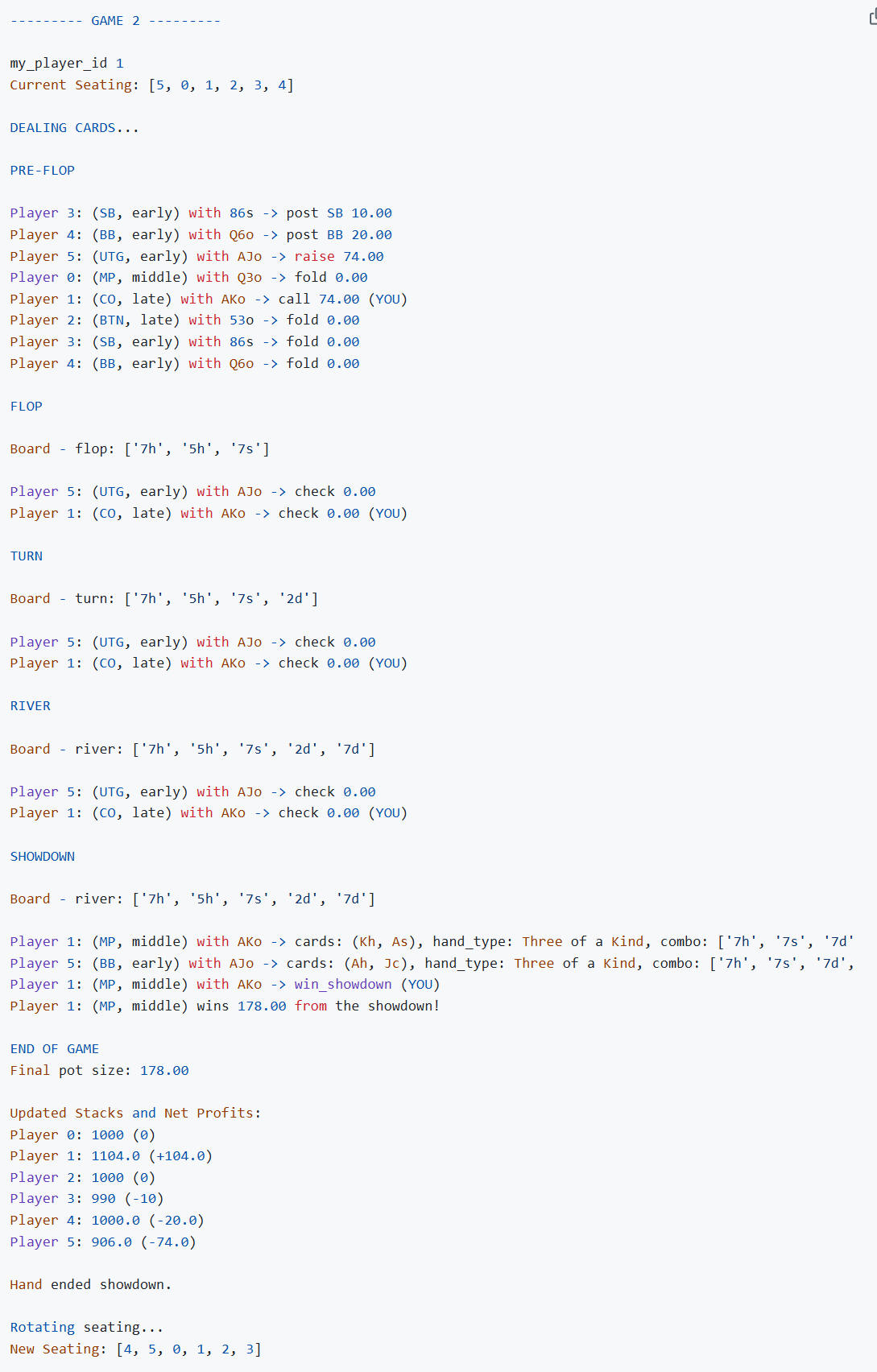

Python Validation Framework for EV and Strategy Consistency Analysis

Independent simulation layer used to validate decision logic, expected value estimation, and distributional outcome consistency across environments.