Gallery

Using Selenium to automate scraping of NVDA financial data from Yahoo Finance

.gif)

Cron scheduling in Ubuntu to run script and update CSV file every minute

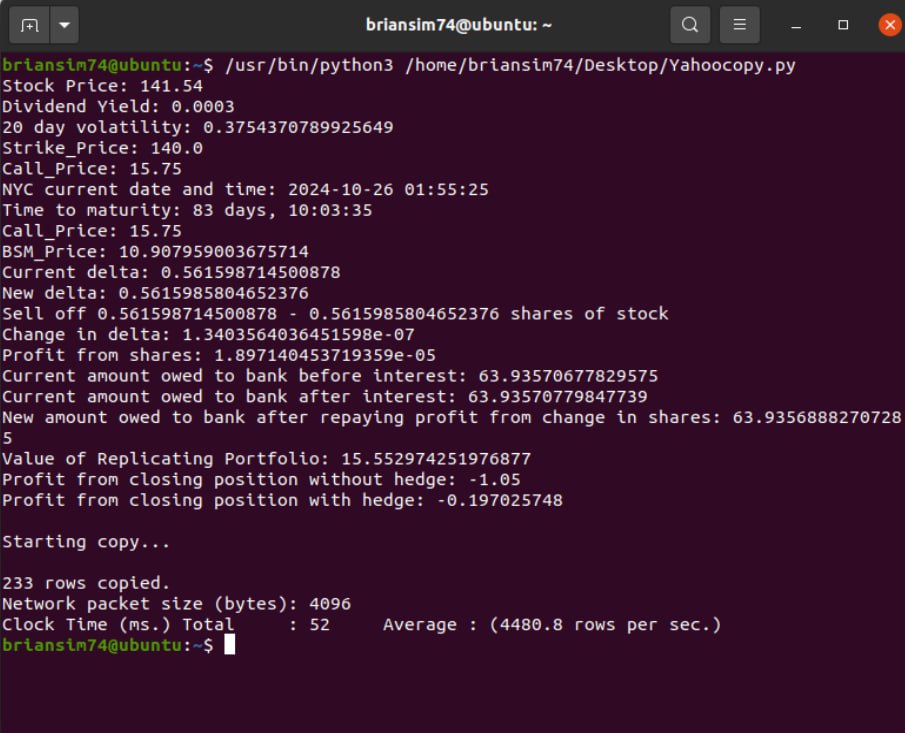

BCP (Bulk Copy Program) Utility to bulk insert updated financial data into Microsoft Azure SQL cloud database every minute

Self adjusting delta position based on current NVDA stock price, option price, time to maturity, etc